How Third-Party Commodity Pool Operators Assist Alternatives Managers with US Regulation

Tightened monetary policy, geopolitical concerns, and residual fear over the pandemic have characterised market volatility in 2022. The subsequent shakiness in the bond and equity markets has led to institutional investors opting for alternative assets to help steer course and provide some portfolio diversification in the form of actively managed strategies.

- Published

- in Analysis & Insights

Within this context, there has been parallel growth in interest for separately managed accounts and managed account platforms to help balance risks inherent in pooled funds. Embargoes stemming from the Russia-Ukraine crisis, metals scarcity and related supply-chain issues, fears over inflation, and volatility in many commodities markets mean that fund managers have a particularly heightened need to keep exposures in check. All the while, funds that trade commodities need to heed US regulatory requirements while proving their worth to the investors that are allocating to these strategies.

What Do Alternative Asset Managers Need to Be Aware of in Commodities Trading?

According to hedge fund industry data source HFR1, alternative assets have experienced the biggest quarterly inflow since second-quarter 2015 and an increase of 81.7 percent compared to the US$10.9 billion in inflows during the same period in 2021. Accounting for a sizeable portion of alternative asset allocations is the managed futures industry.

Statistics from industry data source, Barclay Hedge, show the managed futures industry totalling some US$360 billion as of end-first-quarter 20222, the highest amount over the past 10 years, a period during which the amount of assets in the managed futures industry has shown resilience.

Developments in financial technology and money management, combined with these steep inflows, means industry observers are paying all the more attention to trading strategies for alternative asset classes. Many hedge funds have specialised trading strategies in place for commodities investing, such as futures, options, commodities, physical holdings, and swaps.

While they do have alpha-generating potential, these strategies might fall under the rules and regulations of the US Commodity Futures Trading Commission (“CFTC”); US Commodity Exchange Act (“CEA”); and US National Futures Association (“NFA”).

How Asset Managers and Investors Can Stay on Top of Commodities Trading Reporting Requirements

For many small to mid-size asset managers who often have oversight of portfolio management, operating platforms, and execution of trading strategies, meeting these reporting requirements is beyond their bandwidth. Larger institutional investors may also face challenges. Those that have their own managed account platforms might engage external managers to help execute investment strategies. As such, both commodity trading advisors (”CTA”) and institutional investors alike can benefit from a specialist third-party commodity pool operator (”CPO”) to handle reporting requirements, allowing the CTA to focus on delivering market-beating returns while keeping management fees competitive.

How a Specialist Third-Party Commodity Pool Operator Can Help Fund Managers

CPOs are the corporate governing bodies or professional independent directors of such funds, platforms, and managed accounts. Some directors, subject to certain requirements being met, are able to delegate their CPO responsibilities to the commodity pool’s CTA ; especially when the CFTC registrant CTA has the infrastructure and resources to assume regulatory compliance responsibilities. These responsibilities include annual and periodic NFA flings; where a third- party fund administrator is engaged, substantiating pool performance; satisfying proficiency requirements including certain ongoing training, and being subject to NFA compliance examinations.

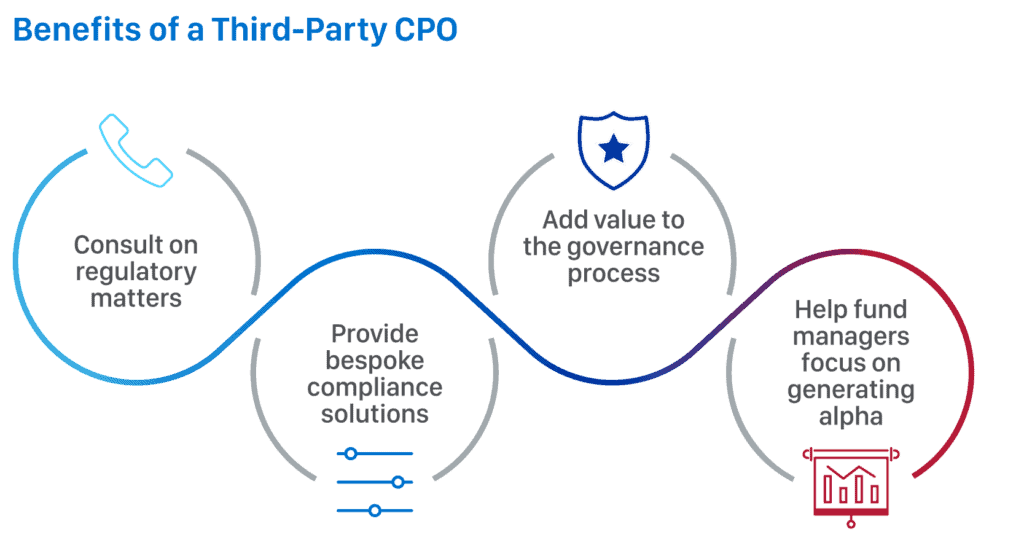

A specialist third-party CPO can bring a layer of governance to portfolio management that can give CTAs and investors the peace of mind necessary so that the CTA can concentrate on alpha generation. A third-party specialist CPO can consult on regulatory matters as they arise, as well as tailor compliance solutions for the fund to adhere to CFTC and NFA rules. Even in situations where a CTA may qualify for certain exemptions, such as a small advisor, from having to register with the CFTC as a CTA, a specialist third-party CPO can provide value. One way is by serving as the CPO where the governing body of the commodity pool or its delegate is CFTC registered. This scenario arises when a small advisor implements a trading strategy that would trigger CFTC registration requirements.

Commodity Pool Operator Compliance Services at the Maples Group

As a leading global fiduciary services provider, the Maples Group works with both well-established and emerging investment advisors on many types of investment vehicles including commodity pools, as well as with independent fund directors to provide assistance with meeting commodity pool compliance requirements.

Our own independent directors and qualified Series-3 professionals provide tailored governance solutions to manage and support CFTC registration requirements, regulatory reporting and ongoing compliance for investment vehicles and managed accounts that are subject to relevant rules and regulations where investors are qualified eligible persons. Where eligibility requirements are satisfied for CFTC registration exemption, our experienced team can also manage the initial and ongoing required exemption and annual affirmation filings with the NFA.

Benefits of a Third-Party CPO

With geopolitical and futures market forces buffeting commodities trading, fund managers of all sizes can benefit from the compliance assistance that a specialist third-party CPO can provide.